How Bossard's TCO Model Could Help These 3 Companies Cut Costs

Are you wondering how TCO could help your company save costs in C-parts management? Here’s an analysis of a few sample companies from 3 different industries. We’ll explain how our TCO model could help each company make decisions to save them money when it comes to C-parts management.

The Importance of TCO in C-Parts

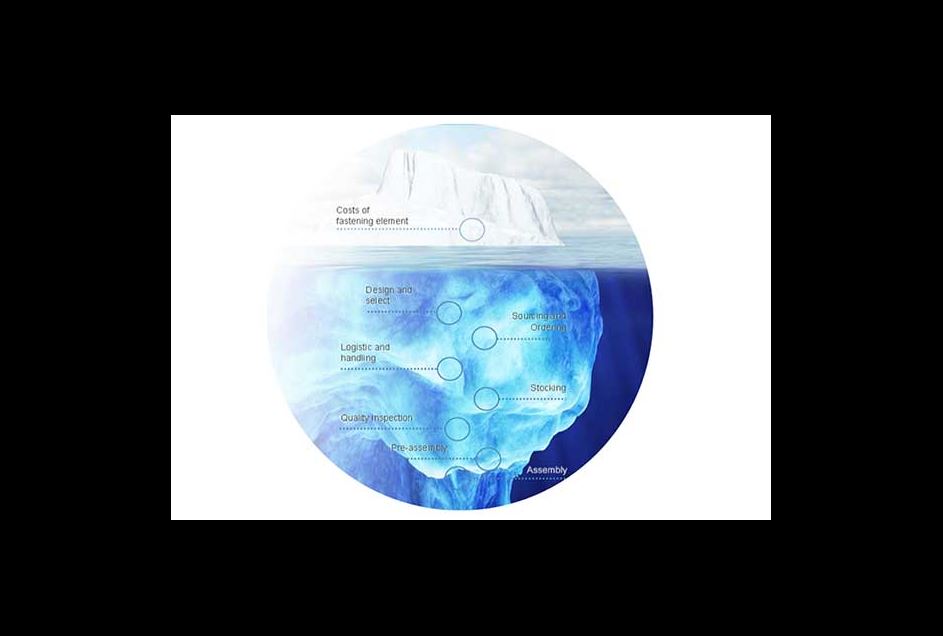

Many companies do not look beyond the purchasing price of C-parts. They don’t realize that they can save money on C-parts because they only see the purchasing price, which is very low compared to other parts. However, Bossard has found that on average, the fastener itself is only about 15% of the total cost involved. The other 85% is spent on the rest of the C-parts ecosystem: design, sourcing, ordering, logistics and handling, quality inspection, stocking, testing, pre-assembly, and assembly. These categories are all full of hidden cost drivers. No wonder there is so much opportunity for cost savings in C-parts!

We decided to take a look at these 3 companies and determine the following:

- The organization’s main goals

- How they use C-parts

- How many suppliers they use

- How they choose suppliers How they order C-parts

- How they approach TCO

- And most importantly, how TCO could help them.

1. A Large, International Coffee Machine Developer / Manufacturer

This company is a worldwide partner of multiple brand suppliers, and they develop and manufacture coffee machines and associated devices. They produce everything from small components to whole machines. They have five production sites, 30 years of experience, and many customers and markets around the world. They strive to manufacture innovative devices, use advanced production methods, and produce high-quality products.

This company has worked with the same suppliers for a long time. They are happy with their two main C-part suppliers, and they maintain that the service, quality, and reliability of these suppliers outweighs the potential cost savings they could get if they switched suppliers. They only explore procurement markets on a reactive basis.

This coffee machine company mainly uses standard C-parts, but the standard assortment is volatile, so new parts are frequently added. The company believes that this is the biggest cost driver in their C-parts management, but they have not calculated their costs here. They do have a fully automated logistics system, but they are not sure how much it saves them.

This company knows about TCO but doesn’t put it into use in C-parts management. They have taken steps to improve parts ordering, as noted above, but have not yet taken logistics, its administration and the non-automated assembly into consideration.

Though this company is doing well in certain areas, it hasn’t tapped into active C-parts management for cost savings. Bossard’s TCO process could help the coffee machine company increase transparency, show where lean management could be implemented, and influence purchasing strategy in the long term. If this company’s R&D management took the time to fill the appropriate numbers into a TCO tool, cost drivers would become apparent and they could adopt leaner practices accordingly.

2. A Global Farming Enterprise

This farming enterprise works around the globe to develop, manufacture, and distribute many different types of agricultural solutions. They have over 3,000 independent dealers and distributors in 150+ countries, and they work to customize every product based on customer needs.

This company has a huge number of C-part suppliers: approximately 1,000 worldwide. Like most manufacturers, they seek the best price offering, quality, and delivery performance when it comes to choosing suppliers. Different sites often use different suppliers and products. One interesting thing about this company is that some of its fasteners are so expensive that they don’t even qualify as C-parts.

They completely outsource C-parts management, and they also have dedicated employees to work with C-parts suppliers. According to the company, their main cost blocks are in logistics, warehousing, refill, and associated IT costs.

TCO is widely used in this company. They have multiple employees whose jobs are to use TCO-conforming practices to estimate the entire costs of every product, and they also calculate real product costs by analyzing each supplier’s procurement, production, and logistics processes. However, these employees focus on A- and B-parts, not C-parts, and C-parts management is outsourced.

TCO is underutilized in this company’s C-parts management. Due to this company’s large size and the volume of C-parts it uses, large cost savings could be made by simply applying TCO to its purchasing decisions, not to mention its production, assembly, quality management, and service decisions.

3. A Well-Established Transformer Corporation

This company researches, designs, and manufactures custom transformers and reactors. They are leaders in the fields of energy distribution, marine, offshore, fixed and mobile rail traction, mining, and renewable energy. They have been in business for almost 50 years.

This company works mainly with a single supplier and uses a Kanban system to order new parts. Their order processing is simple, and their relationship with their single supplier is good. They review their C-parts frequently. This company stands out because 50% of their parts are C-parts, but C-parts only make up less than 1% of their costs.

This company uses a standard assortment of C-parts, which are automatically delivered directly to the company’s warehouse. They have experienced great cost savings here.

The company is familiar with TCO and has applied it to its developed items and the associated life-cycle.

This company is doing well at managing C-parts costs as it applies to order processing, logistics, and standard assortments. However, it could experience greater savings by applying TCO to its production, assembly, quality management, and service to determine hidden costs.

Find out more now with your free E-Book to see how TCO will optimize your C-parts management.How TCO will optimize your C-parts management